I was in attendance at a conference in Denver yesterday when an expert toxicologist suggested that there is evidence of many insurance company wildfire testing companies looking for smoke and toxic residue in all the wrong places. It reminded me of a conference I was at last week in California, where a claims expert warned of insurance companies not fully investigating wildfire smoke, soot and ash claims. I took the above photo of the expert’s slide on the issue.

Los Angeles continues to reel from the devastating effects of recent wildfires. Yet another slow-burning crisis is emerging in their wake. Insurers are failing to fully investigate fire-damaged structures for toxic contamination. This oversight not only jeopardizes the health of homeowners and business occupants, it violates well-established legal duties owed by insurers under both statute and common law.

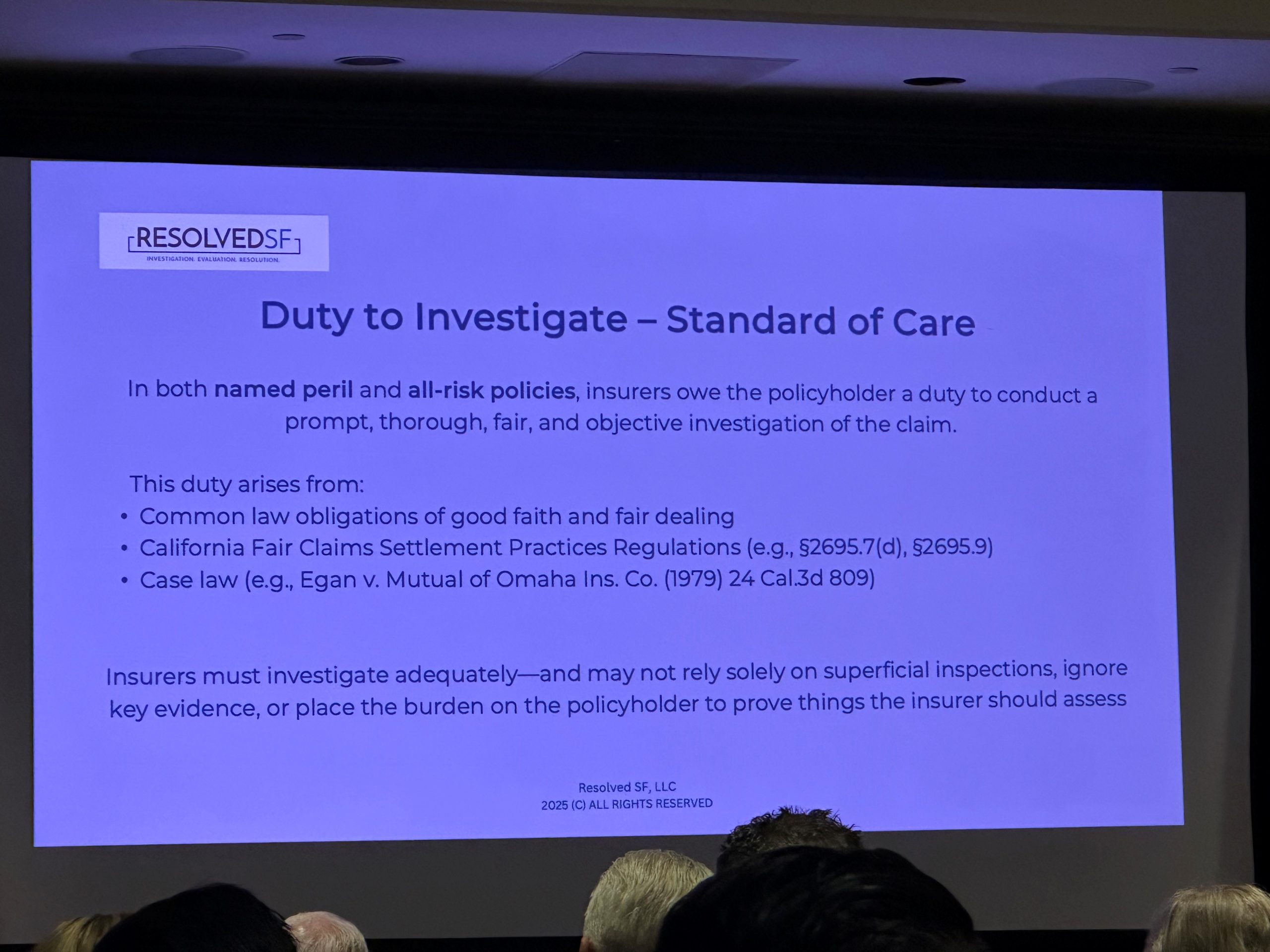

The Legal Duty to Investigate Claims Thoroughly

The law in California is unambiguous. Insurers must perform a prompt, thorough, fair, and objective investigation of all claims. This duty is not optional or flexible; it is rooted in the implied covenant of good faith and fair dealing and codified in California’s Fair Claims Settlement Practices Regulations.

In Egan v. Mutual of Omaha Insurance Company, 1 the California Supreme Court made it clear that a superficial or biased investigation is legally insufficient. The court stated, “an insurer cannot reasonably and in good faith deny payments to its insured without thoroughly investigating the foundation for its denial.”

The insurer’s obligation is not to minimize liability but to proactively protect the insured’s interest. The Egan court emphasized that “To protect these interests it is essential that an insurer fully inquire into possible bases that might support the insured’s claim.”

The Overlooked Threat of Toxic Wildfire Residue

Wildfires are chemical events as much as they are physical ones. When homes, cars, synthetic materials, and plastics are incinerated, they release hazardous particulates and volatile organic compounds that settle into homes and business structures, even those that appear outwardly intact. This residue can be carcinogenic, neurotoxic, and environmentally persistent.

Yet despite the well-documented risks, many insurers have failed to conduct environmental testing or engage industrial hygienists in areas close to the wildfire. Some instead perform only a brief walk-through, ignore persistent odors and residues, and deny additional removal costs unless the homeowner can prove the existence of toxins. But in the eyes of the law, the burden to investigate rests squarely on the insurer, not the insured.

This was precisely the failing identified in Egan. There, the court condemned the insurer’s refusal to consult with the insured’s treating physicians or to order an independent medical exam. The insurer relied on incomplete paperwork and failed to engage in meaningful inquiry. That conduct, the court ruled, constituted a breach of the duty of good faith.

If an insurer cannot rely on shallow documentation to deny disability claims, it likewise cannot rely on superficial visual inspections to dismiss the presence of toxic wildfire residue.

The Egan decision did more than outline duties. It warned insurers of the consequences of breaching them. The court held that bad faith denial of a claim opens the door not just to compensatory damages but punitive damages as well when the conduct is shown to be oppressive or malicious.

As the court noted, “when the insurer unreasonably and in bad faith withholds payment of the claim of its insured, it is subject to liability in tort.” It found that punitive damages could be appropriate when an insurer acted “with an intent to oppress, and in conscious disregard of the rights of its insured.”

In today’s wildfire claims, this raises a serious legal question: Are insurers willfully avoiding testing because the results might require them to pay tens or hundreds of thousands more? If so, they may be acting with conscious disregard, a high standard, but one clearly met in Egan and potentially met in post-fire cases today.

This failure to investigate wildfire claims thoroughly can be aptly compared to the parable of the Three Wise Monkeys: “See no evil, hear no evil, speak no evil.” When insurers perform cursory inspections of fire-affected properties without testing for toxic residue, they are effectively choosing to see no evil. Despite knowing that wildfires involving modern construction materials almost inevitably result in hazardous contamination, some insurers willfully avoid uncovering evidence that might increase their financial liability. In doing so, they engage in a form of deliberate ignorance that courts have recognized as bad faith.

The second monkey, who hears no evil, is embodied by claims handlers who dismiss or ignore reports from policyholders about unusual odors, soot deposits, and physical symptoms. Rather than commissioning appropriate environmental or health assessments, they decline to consult toxicologists or industrial hygienists. This refusal to listen runs contrary to the insurer’s duty under Egan to fully inquire into possible bases supporting the insured’s claim. Turning a deaf ear to credible evidence and expert warnings is not merely unprofessional, it is potentially unlawful.

Finally, the third monkey, who speaks no evil, represents the suppression or avoidance of critical facts. Insurers may decline to inform policyholders of the potential for toxic contamination or fail to explain that specialized testing is needed. Some may offer “final” settlements without disclosing what was and was not assessed. This silence deprives insureds of the information they need to protect themselves and challenge incomplete or misleading claim evaluations. In this way, the insurer’s duty to communicate openly and in good faith is undermined by a calculated choice to remain silent in the face of harm.

The California Supreme Court in Egan highlights that the relationship between insurer and insured is inherently imbalanced. Insurance contracts are not commercial transactions between equals. Instead, they are instruments of trust, purchased to provide peace of mind in crisis. The court recognized that “the purchase of such insurance provides peace of mind and security” and that insurers must act with decency and humanity inherent in the responsibilities of a fiduciary.

Homeowners whose properties have survived fire but are steeped in toxic residue are not out of danger. Their homes may be uninhabitable, and their insurance policies should serve as their shield. When insurers shirk their duty to investigate, they do more than breach a contract, they may jeopardize lives and violate the law.

As the aftermath of California’s wildfires plays out, the public and legal community must remain vigilant. Insurers must not be allowed to cut corners when public health and legal obligations are at stake. The law, as articulated in Egan, demands more than bare minimum compliance. It demands integrity.

The next time a claims adjuster or spokesperson for an insurer shrugs off concerns about lingering odors, black dust, or unusual health symptoms, they should be reminded of what the California Supreme Court said more than four decades ago: “an insurer may breach the covenant of good faith and fair dealing when it fails to properly investigate its insured’s claim.”

Thought For The Day

“Facts do not cease to exist because they are ignored.”

Aldous Huxley