Stemming from the McCarran-Ferguson Act of 1945, insurance is regulated by the states. Knowing variations of the law and regulations is a necessity for insurance professionals crossing state lines. These state-by-state variations in law include the basics, such as determining replacement cost and actual cash value.

Check out Chip Merlin’s recent blogs, The Devil Is in the Details When Making a Claim with Church Mutual Insurance Company, and California Requires Actual Cash Value Payment By Code, to better understand why this topic is ripe for discussion.

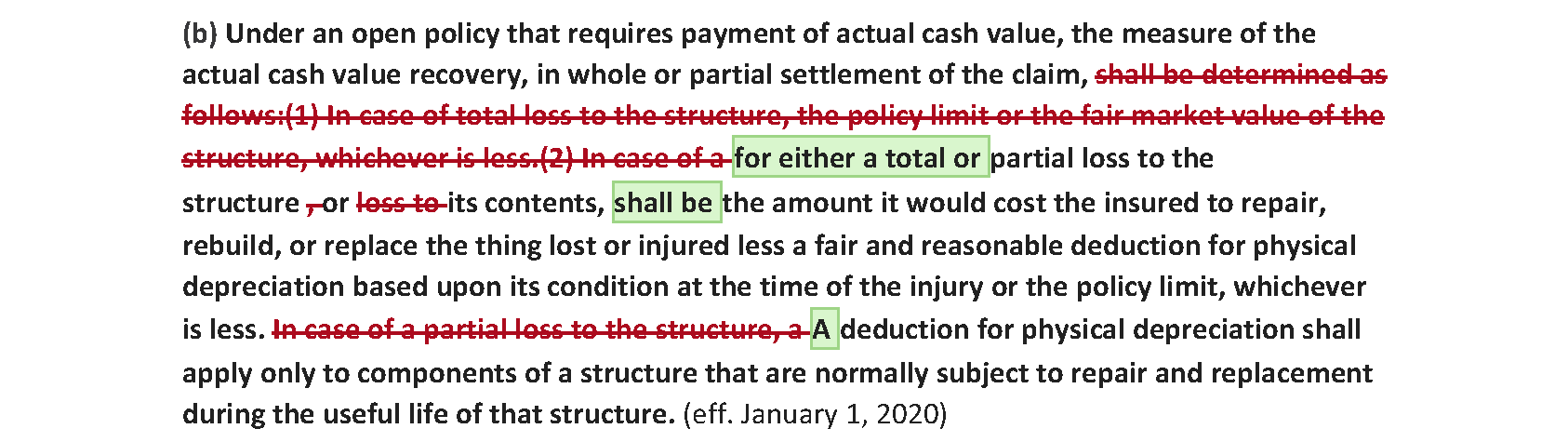

Specifically, this blog follows up on Victor Jacobellis’ March 2019 post, Applying Depreciation in California – Understanding the Guidelines. At the time of Victor’s blog post, the California legislature was drafting a bill that has since been codified with an effective date of January 1, 2020. Essentially, it amended California Insurance Code § 2051 to require a uniform method of determining Actual Cash Value for a structure and personal property, regardless of whether there was a total or partial loss: Actual Cash Value = Replacement Cost – Depreciation. This was a monumental shift away from allowing a fair market value assessment of structures for total losses – a method leaving many policyholders underinsured since rebuild costs frequently and predictably exceed the fair market value of a home. This is especially true when accounting for demand surges after a widespread disaster. Here is a comparison of the prior §2051 language (stricken) and current language (highlighted):

To assist in the determination of what constitutes a “fair and reasonable deduction for physical depreciation,” California has adopted guiding regulations, which also provide protections for policyholders. 10 CCR 2695.9(f) states:

(f) When the amount claimed is adjusted because of betterment, depreciation, or salvage, all justification for the adjustment shall be contained in the claim file. Any adjustments shall be discernable, measurable, itemized, and specified as to dollar amount, and shall accurately reflect the value of the betterment, depreciation, or salvage. Any adjustments for betterment or depreciation shall reflect a measurable difference in market value attributable to the condition and age of the property and apply only to property normally subject to repair and replacement during the useful life of the property. The basis for any adjustment shall be fully explained to the claimant in writing.

(1) Under a policy, subject to California Insurance Code Section 2071, where the insurer is required to pay the expense of repairing, rebuilding or replacing the property destroyed or damaged with other of like kind and quality, the measure of recovery is determined by the actual cash value of the damaged or destroyed property, as set forth in California Insurance Code Section 2051. Except for the intrinsic labor costs that are included in the cost of manufactured materials or goods, the expense of labor necessary to repair, rebuild or replace covered property is not a component of physical depreciation and shall not be subject to depreciation or betterment.

Four aspects of this regulation section require further attention. First, a policyholder or policyholder advocate must not face an uneven level of information when negotiating a claim involving adjustments for depreciation, often an imperfect science. In California, insurers are required to record and share their justifications, in writing, as to the basis for any discernable, measurable, itemized, and specific dollar amount of any adjustment. This burden lies with the insurer, not the policyholder.

Second, a depreciation adjustment in California must reflect a measurable difference in market value based on both age and condition. While many states may allow for insurers to rely on depreciation charts based solely on age, California requires the property’s condition to be taken into account. Thus, no one size fits all application should be utilized. For example, Grandma’s 20-year-old couch that had a plastic cover on it may be subject to less depreciation than the one-year-old couch owed by the family with five young kids and three pets. It is useful to remind adjusters that the condition must be considered, especially if they are from out-of-state.

Third, the regulation reiterates language in the statute that allows depreciation only to property normally subject to repair and replacement during the useful life of that property. Thus, property components, such as the foundation, should not typically be subject to an adjustment for depreciation.

Finally, in recent years, courts throughout the country have been determining whether insurers in their states can depreciate labor when calculating actual cash value. In fact, we have quite a few blogs on the subject.

California has shortcut the uncertainty and makes clear in its regulation that “the expense of labor necessary to repair, rebuild or replace covered property is not a component of physical depreciation and shall not be subject to depreciation or betterment.”1

Don’t leave depreciation proceeds owed on the table. Request justifications for depreciated items, provide evidence of the condition of your structure and personal property, and do not accept depreciation adjustments for property not subject to it or labor costs.

_______________________________________

1 Cal. Code Regs. 10 CCR 2695.9(f)(1).