I have spent decades in the trenches of property insurance claims disputes. I am going to say something plainly that many inside the insurance claims industry quietly acknowledge but rarely say out loud. The worst conduct in claims handling does not come from the rare bad actor policyholder. Instead, it now comes from a claims system that too often tolerates, and sometimes incentivizes, obstinate adjusters, outcome-driven vendors, and a culture of delay and denial.

That is not a comfortable statement. But it is an honest one.

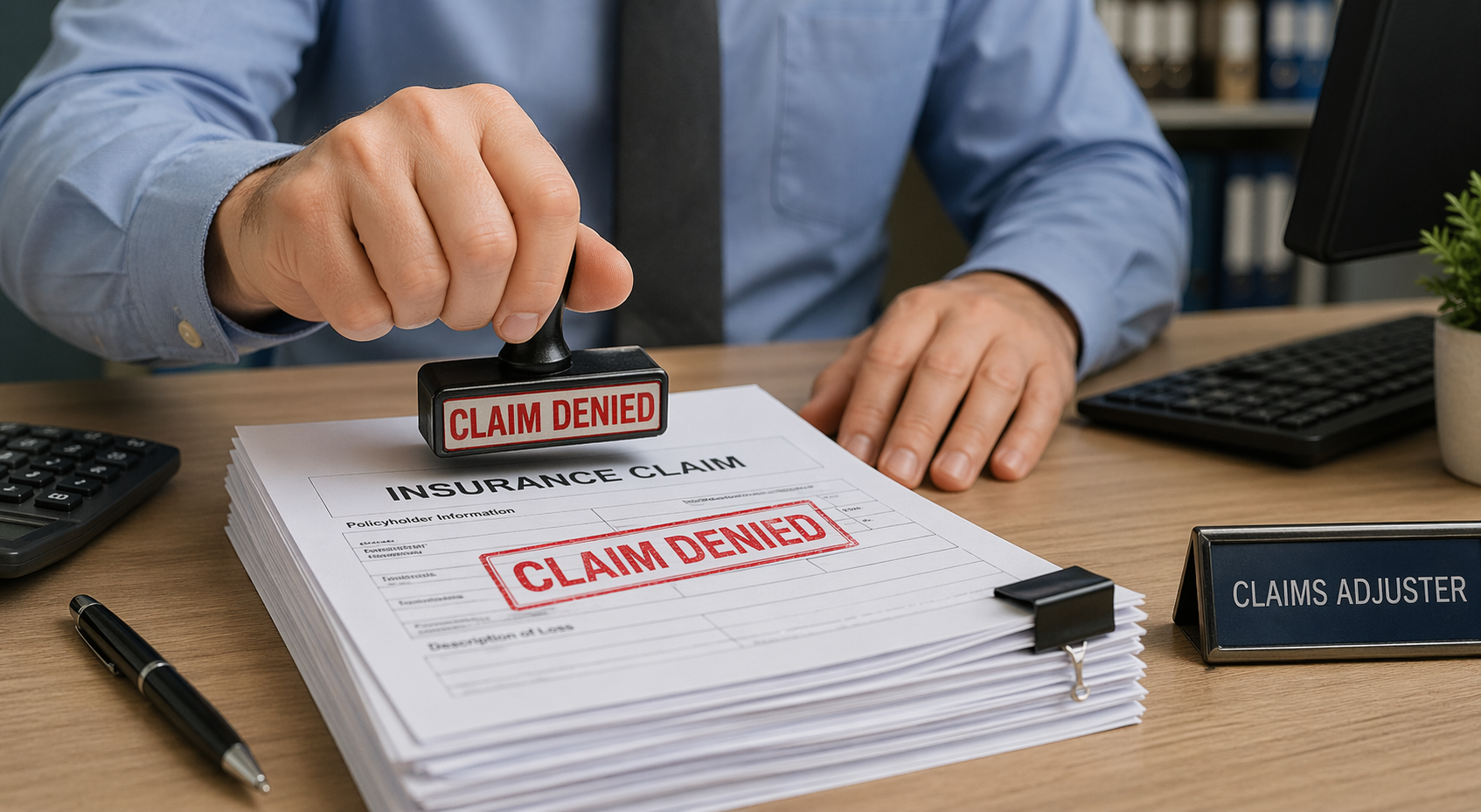

Across the country, I see patterns repeat themselves with alarming consistency. Claims are under-scoped. Engineers are retained who seem to find “no damage” with remarkable regularity. Adjusters who are retained by insurers or who are company adjusters dig in their heels rather than adjust the claim and look to help their customer. Indeed, I rarely find internal claims guidelines suggesting that adjusters agree to look for benefits owed but overlooked. Instead, policy language is stretched beyond reason to avoid payment. When challenged, the system slows down, hoping the policyholder runs out of time, money, or patience.

If the insurance industry and its state insurance regulators truly want to improve public trust, they should stop issuing polished reports and start doing something far more meaningful. Listen and take action. I am talking about a broad, transparent, public forum where policyholders and even honest company or independent adjusters can come forward and explain exactly what is happening on the ground. Not sanitized testimony. Not curated panels. Real stories. Real files with real conduct.

Right now, the truth is being lived and not reported. I hear reports of and see files, especially in Texas, where the adjustment no longer takes place.

Let me be even more direct. In my current practice, Texas stands out, and not in a good way. I challenge anyone to show me a jurisdiction where the combination of aggressive claims practices, regulatory inaction, and insurance contract interpretation is producing worse outcomes for policyholders. I would welcome that debate because it would mean we are finally having the right conversation. Texas sucks if you are a policyholder with a claim.

What are Texas insurance regulators doing when patterns of underpayment emerge? What happens when the same Texas insurance vendors repeatedly minimize damage findings? Where is the scrutiny when entire categories of claims appear to be systematically discounted?

If Texas insurance regulators are being candid, they will admit that enforcement actions are too few, too slow, and too reactive. Market conduct exams often come years after the damage is done. By then, the policyholder has already absorbed the loss, financially and emotionally.

Here is the uncomfortable truth for the insurance claims industry. Most claims adjusters are not bad people and want to help people in their time of need. But many are now operating within a system that rewards minimizing payouts and discourages independent judgment, and prevents them from doing what is right for the insurance customer. When you combine that with insurance expert vendors who understand which conclusions lead to repeat assignments, you create an environment where fairness is no longer the default. Instead, it is the exception. Texas leads the nation in this claims problem.

That is not insurance but a managed outcome. The solution is not complicated, but it requires courage.

Open insurance company internal operation guides, bulletins, and financial incentives for objectives of action and outcomes. Regulators should invite suggestions for scrutiny and then conduct deep searches into the power around and motives within the claims departments. Texas should create a forum where any employees of the insurance company can speak freely without fear of retaliation about their mission to fully pay policyholders. I challenge leaders in the insurance industry to explain why this is wrong or not in the public’s interest.

Let sunlight do what internal memos never will. If the industry believes it is getting it right, it should have nothing to fear from transparency. If regulators believe they are holding carriers accountable, they should welcome the opportunity to prove it in the open.

If I am wrong about Texas, or any other state, I invite those who believe otherwise to step forward and make the case. Show us the data. Show us the enforcement. Show us that policyholders are being treated with the good faith the law requires. After reflection about being too silent or too non-controversial, where I sit today, representing policyholders from coast to coast, the stories tell a very different tale.

Insurance is supposed to be a promise. Right now, too often, it feels like a negotiation and one where the deck is stacked.

I wish to thank Adam Brenner for inspiring me to write this post. Adam called me about my position for raising the public adjuster standards, as I suggested recently in The Public Adjusting Crossroads: A Wake-Up Call the Profession Cannot Ignore, and Will the Public Adjusting Profession Rise to the Occasion. He suggested that I was not fully explaining the most important issue about insurance company misconduct. I agree.

And to be fair, I would suggest that there are companies with a great claims culture. The current leader is AMICA. It wins in our votes taken from public adjuster groups and even insurance industry groups.

Thought For The Day

“The truth will set you free, but first it will make you uncomfortable.”

— James A. Garfield