When it comes to business interruption and extra expense coverage, many think of this insurance as a safety net, but how tangled that net becomes after a loss can impact your bottom line and viability.

RIMS, The Risk Management Society™ published a new 2017 survey from businesses who have suffered BI losses and information from various risk managers. RIMS developed a working group of underwriters, accountants and brokerages to document business loss issues include adequacy of coverage and problems with claims.

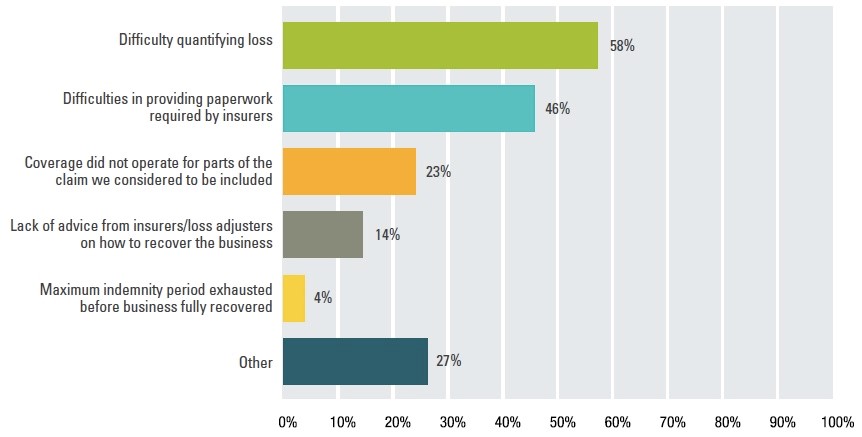

- 58% who have been through a claim said “difficulty quantifying loss” was the biggest challenge they faced;

- 39% indicated their existing BI policy provides either insufficient or no coverage for cyber risk, while 10% were unsure whether the policy covered cyber risk; and

- 35% have 12 months as the length of the maximum indemnity period (working group experts report 12 months is rarely an adequate timeframe).

This data shows many risk managers are not satisfied with the coverage. One shocking finding was how poorly insurance set forth adequacy of values and limits. If the risk managers who are intimately familiar with a loss are ranking adequacy this low, it tells business owners that a quick review once a year of your insurance is not enough.

- In all, just 17% of surveyed risk managers reported they were “extremely confident” that their BI values and limits are adequate. On the other end of the scale, 11% of respondents characterized themselves as having no confidence, with the middle ground (no confidence to extreme confidence) occupied by two groups (29% and 42%).

Another troubling factor was that nearly half of those who responded cited difficulty with providing the documentation required by the insurers. These difficulties included multiple requests for the same documents, requests for documents that don’t exist, unclear requests from carriers who aren’t familiar with the business or businesses, and the turnover of adjusters.

Insurance companies can do a much better job with explaining the basis of what they need and making clear and concise requests in a timely manner. Policyholders also must know that document production can be an overwhelming responsibility that may require dedicated attention and time that is normally allocated to the business. The nature of the requests may require not only the hiring of counsel or a dedicated policyholder public adjuster, but also time is needed by the principles to ensure that a proper production and searches are done. The problem that many face, as the survey reflects, is that even when you have spent the time and produced the information, the insurance company may not be satisfied and the claim remains stagnant with little communication from the carrier. They may make off-base demands but there is rarely the assistance and service you expect in your time of need.

Businesses need to make sure they consult with experts in this field and press forward with due diligence to resolve the matter, understanding that the avenue to resolution may require counsel well versed business losses.

For other popular blogs about BI coverage check out: