There is little doubt the first-party property loss industry is ever-changing. Each year policyholders, contractors, mitigation specialists, public adjusters, and attorneys must adapt and pivot to changes that are strategically launched by the insurance industry. This statement isn’t intended to sound cloak and dagger – it’s just true. In fact, it is common knowledge insurance carriers pay millions of dollars per year to think tank consulting companies like McKinsey & Co., Accenture, Boston Consulting Group, and Bain & Co., who evaluate claims processes and suggest company-wide strategic initiatives for cost-saving purposes under the guise of improving customer service.

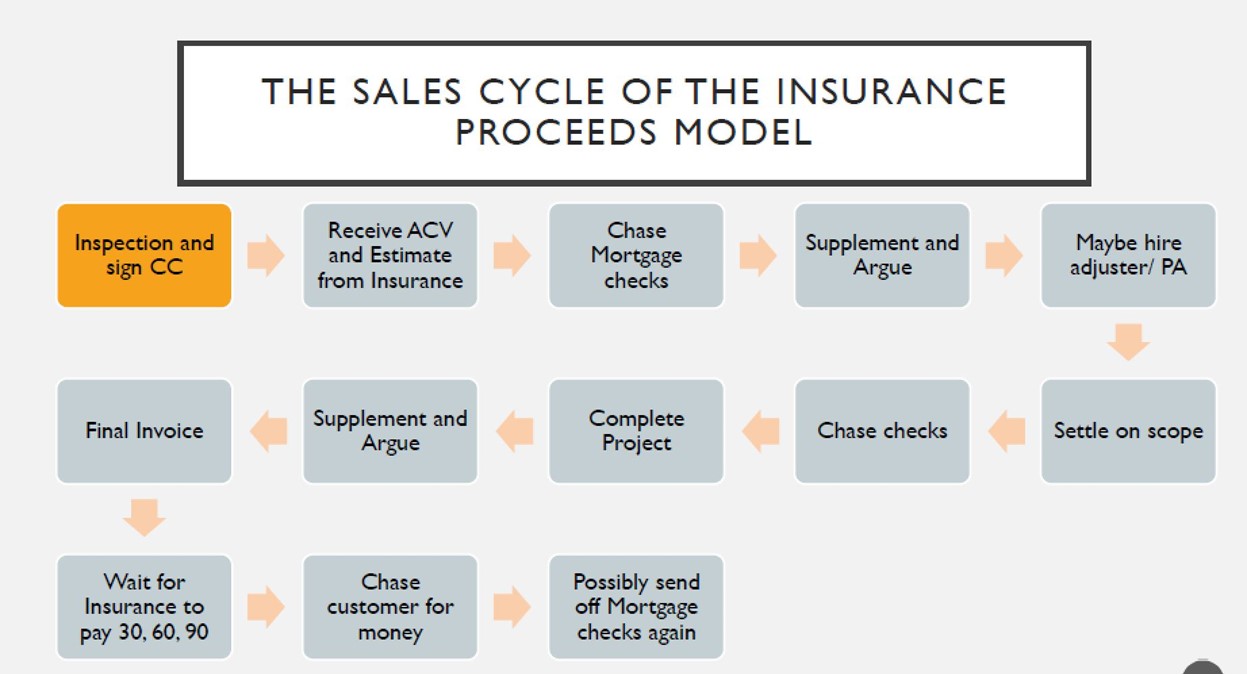

Arguably, the present-day “insurance proceeds model,” as Jen Silver commonly calls it, is one such example of the deliberate control that insurance companies maintain over the claim process. After all, doesn’t the following sales cycle look familiar for nearly every claim that a policyholder files, regardless of the insurance company involved?

There can be no dispute the insurance proceeds model benefits only the insurance carriers. What if something could be done to circumvent this typical sales cycle and the routine claim process everyone has become accustomed to. According to Jen Silver, there is – and it’s working.

Chances are, if you have not met Jen Silver or seen her speak, you have at least heard of her. By promoting her retail method and going against the status quo for insurance claim estimates, Ms. Silver has quickly risen to stardom, and rightfully so. Having spent some time with Ms. Silver and watched her presentation on the retail model, it is very interesting to witness the change in her audience by the time she is through. To be sure, the retail sales model for contractors is not a new idea and for many contractors, the knee-jerk response that it “won’t work” or “just isn’t how we do things here” is expected. However, midway through her presentation, when the lightbulb goes on and attendees start to connect the dots, you can feel the room change. I sensed it, and I’m not even a contractor! Interestingly, it’s the simplicity of Ms. Silver’s retail model that seems to resonate with contractors as she explains it in a very humble “I’m just a roofer, and I am not ashamed to admit it” kind of delivery. So, if you want to hear Ms. Silver speak firsthand about her retail model, I encourage you to attend her event on February 28, 2022, in Dallas, where she, Steve Patrick, Steve Badger, Chuck Thokey, and Reggie Brock will be speaking about “One Industry One Model.”

Although the retail model and Ms. Silver’s “One Industry One Model” event is primarily focused on contractors, it works for everyone, and the net result of a “cost incurred” policyholder is what I find most interesting from a legal standpoint. To illustrate, consider the contractor who follows a retail model and signs with a policyholder to replace their damaged roof as a result of a known hailstorm (April 28, 2021, in Norman, OK, comes to mind). For a myriad of reasons all of you reading this blog have probably heard in the past, the carrier wrongfully underpays after coverage is extended. Despite the insurance carrier’s disputed position, the contractor stays out of the claim process, and the policyholder decides they are not going to wait around fighting for the insurance proceeds to replace their damaged roof. Instead, the policyholder obtains financing or pays out-of-pocket to fix the damage, and the contractor does the work pursuant to the reasonable price in their retail bid. When this happens, the result is a “cost incurred” policyholder. I would suggest these are very risky policyholders for insurance companies to deal with because as long as the contractor’s charged amount was reasonable and in line with industry standards, the “Loss Settlement Provision” of most insurance policies requires the insurance company to reimburse the policyholder for the “costs incurred.” If they don’t “Pay Up!” then you now have a policyholder who has mitigated their loss by replacing the damaged roof (out-of-pocket or through financing), thereby sustaining actual damages in support of a breach of contract claim under the policy. Moreover, the risk to an insurance company increases considering a jury could find its initial failure to pay the claim, coupled with the subsequent failure to reimburse the policyholder for “costs incurred” is tantamount to bad faith and/or punitive damages depending on the jurisdiction. The generalized distinction is a policyholder who has incurred the costs versus the policyholder stuck in the insurance model simply waiting on the insurance proceeds to do the work are (and rightfully should be) viewed vastly different by an insurance company who is always evaluating the “risk” associated with any particular claim. Thus, the rapid paradigm shift that a retail model approach can cause is very promising toward leveling the playing field for policyholders.

Quote for the Day

It is not the strongest of the species that survive, nor the most intelligent, but the one most responsive to change.

—Charles Darwin