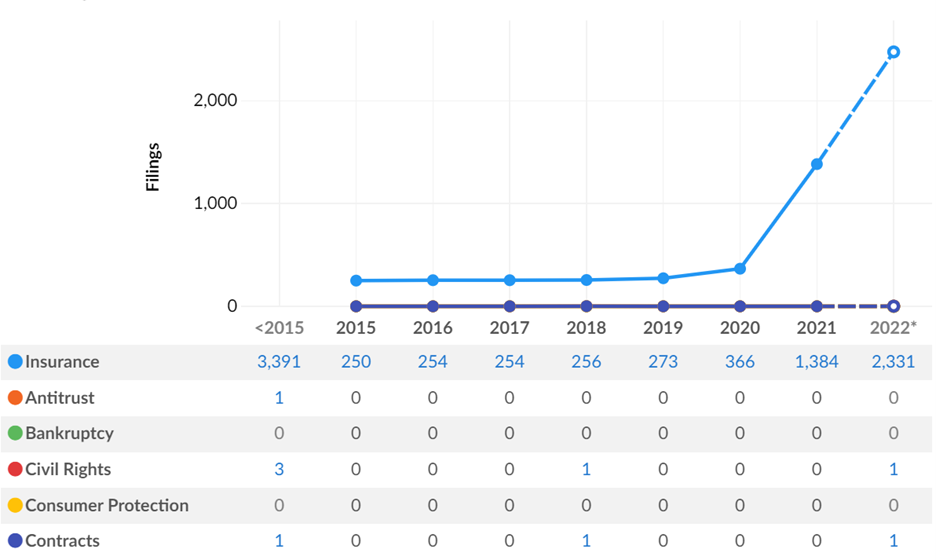

In Oklahoma, we’ve been keeping a close eye on State Farm Fire and Casualty Company and its claims handling practices, as it seems something within State Farm has changed, making litigation against it more frequent. This graphic depicting the trajectory of insurance-related lawsuits involving State Farm in federal courts throughout the country is telling:1

One case we’ve kept a particular eye on is Bates v. State Farm Fire and Casualty Company,2 which is pending in the Western District of Oklahoma. On November 7, 2022, after a five-day jury trial and nearly six hours of deliberation by the jury, the jury rendered a verdict finding State Farm breached the insurance contract and failed to act in good faith and with fair dealing towards its insured, Mr. Bates. In doing so, the jury awarded $15,800.00 for breach of contract damages and $325,000.00 for State Farm’s bad faith conduct.3

At trial, the jury heard evidence of a significant hailstorm hitting the Plaintiff’s rental property and damaging the Plaintiff’s roof. State Farm investigated the reported damage by sending a then-brand-new adjuster to inspect the home. This adjuster lacked any real-world experience assessing or investigating hail damage, having only recently completed her initial training with State Farm, which was entirely virtual except for the few roofs she inspected with another adjuster. Of the roofs she had previously inspected with the other adjuster, none were found to have hail damage. The adjuster in Bates found covered hail damage to the soft metals of the home but not to the shingles. This decision prompted Plaintiff’s representative to request a reinspection by State Farm with an experienced adjuster. State Farm refused to grant the reinspection. The jury further heard evidence of multiple mistakes made by the adjuster, including a miscalculation of the depreciation applied in State Farm’s estimate of damages and a failure by State Farm to pay for a mailbox and other soft metals State Farm agreed were damaged by hail and covered by the insurance policy.

Importantly, the jury also heard testimony from a former State Farm adjuster with more than 13 years of experience adjusting property losses. She testified about a training initiative known as “Hail Focus.” According to this adjuster, when Hail Focus was initiated, her direct supervisor and Team Manager stripped her of her ability to approve payment of roof replacements without first obtaining approval from the Team Manager. This meant she could not chalk areas of the roof she felt were damaged by hail until first speaking with the Team Manager; she could not approve payment for a roof replacement on-site during an inspection unless first obtaining approval from the Team Manager; and she could not tell property owners, contractors, or public adjusters of her decision to pay for the roof until she first obtained approval from the Team Manager. At trial, the Team Manager, who is notably now a Section Manager, denied knowledge of the Hail Focus initiative. The Section Manager provided similar trial testimony.

The Bates verdict came only a month and a half after a different Oklahoma jury found State Farm breached an insurance contract with its insureds and failed to treat its insureds in good faith. In Rowan v. State Farm Fire and Casualty Company, an Oklahoma County jury awarded the Plaintiffs $70,400.00 for State Farm’s breach of contract and $680,000.00 for State Farm’s bad faith conduct.4 In Rowan, a storm ripped the Plaintiffs’ roof from their home and damaged the interior of the home and the home’s contents. State Farm determined the home suffered no structural damage; ignored the Plaintiffs’ repeated concerns regarding the home’s electrical wiring; conducted an outcome-oriented investigation into the Plaintiffs’ claim; and retained biased consultants to support State Farm’s position.

Needless to say, State Farm’s claims handling conduct rightfully deserves scrutiny. Like all insurers in Oklahoma, State Farm is prohibited from unreasonably, and in bad faith, withholding payment of a claim owed to its insured.5 If State Farm delays issuing payment to its insured, then it must have a reasonable basis for doing so, and it must also treat its insured fairly and in good faith.6

______________________________________________

1 Source: Lex Machina

2 Bates v. State Farm Fire & Cas. Co., No. 5:21-cv-00705 (W.D. Okla.).

3 Bates v. State Farm Fire & Cas. Co., No. 5:21-cv-00705 (W.D. Okla. Nov. 7, 2022).

4 Rowan v. State Farm Fire & Cas. Co., Oklahoma County Case No. CJ-2017-7301 (Okla. July 27, 2022).

5 Christian v. Am. Home Assurance Co., 577 P.2d 899, 905 (Okla. 1977).

6 Ball v. Wilshire Ins. Co., 221 P.3d 717, 724 (Okla. 2009).