Florida insurance companies have been notorious for increasing rates and filing news articles at the start of legislative sessions that support their legislative propaganda efforts. The typical scapegoats are lawyers and contractors. Somebody from the Attorney General’s office and newspaper reporters should call the lawyers for a contractor regarding a complaint1 filed and follow with an investigation about a lawsuit which states:

29. Instead of ensuring that field adjusters created honest, accurate reports to confirm that UPC’s insured received an assessment that reflected their loss, Defendants specifically instructed desk adjusters to modify the estimates created by field adjusters to decrease estimates in order to ultimately decrease the amount of money UPC pays to its insureds when claims are made under the insurance policies. In many circumstances, Defendants instructed field adjusters to modify reports to give UPC a “factual basis” to deny coverage altogether. Defendants pressured adjusters to create factual bases that were fraudulent in order to deny claims.

30. As this scheme has come to light, some field adjusters have stated under oath that UPC commanded them to add language to their reports which was inaccurate and outright false.

Allegations of a lawsuit are just allegations and not the truth. But, after reading the following, I feel many people should follow up with what is going on and why this type of behavior is tolerated:

Rod Buvens, a field adjuster acting on behalf of UPC through PLS following Irma, testified that UPC’s desk adjuster instructed him to add language into his report “[t]hat no wind damages were observed upon inspection” at the property at issue, despite this language being categorically false based upon Mr. Buvens’ own inspection of a property.

Relating to homes damaged by Irma, Mr. Buvens advised UPC’s desk adjuster, Josh DeMint, numerous times that the statement “no wind damages were observed upon inspection” was incorrect multiple times; yet, Mr. Buvens was still required to include the categorically false statement in his report at the demand and instruction of UPC.

Mr. Buvens testified that UPC demands its field adjusters remove items from an estimate, which ultimately results in UPC owing less to its insureds. 34. For example, Mr. Buvens testified that he was specifically instructed to remove portions of his estimate, which would have amounted to an additional $1,376.30 that UPC would have owed pursuant to the insurance policy. Moreover, if Mr. Buvens’ report and estimate were not wrongfully modified by UPC, the insured in this specific instance would have obtained a full roof replacement, which would have cost UPC thousands of dollars more pursuant to the insurance policy.

I strongly urge all policyholders with UPC claims to make reference to this alleged conduct and get this evidence.

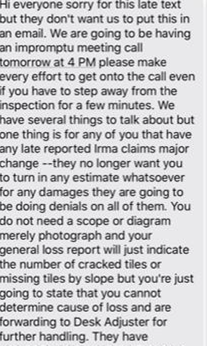

How about policyholders who did not climb on their roofs after Hurricane Irma and later reported leaking roof problems with UPC? How were they treated? Look at this secret text:

When the truth comes out, can anybody really trust Florida’s insurance company claims executives and their lobbyists about what they do to pad their profits and not pay claims?

I am on the Board of the American Policyholders Association. One of its missions is to recognize insurance fraud:

The APA recognizes that at the time of loss, property owners rely upon the insurance companies and their agents to measure the loss to a property and determine what the insurance company is obligated to pay in benefits. The property owner and insurer have adverse interests in the determination of an insurance company’s liability. The APA studies the conflict of interest present in the adjustment process and monitors the systematic methods used by the insurance industry to determine policy benefits. The APA recognizes that insurance fraud occurs far too often by those obligated to pay for the loss.

I trust that its APA investigators will be calling me about this case. This is what happened in Superstorm Sandy, where insurance company retained expert reports were changed because of pressure to help the insurance company pay less than what was owed.

One thing is certain—either this lawsuit, which is backed up with sworn testimony, is wrong, or a major Florida insurance company is engaged in fraudulent conduct. Based upon allegations in sworn testimony, it would seem that Ashley Moody, in her capacity as Florida’s Attorney General, should look into these allegations to see if they have merit.

Another question is whether Florida’s insurance commissioner will do anything about this once it is brought to his attention. He seems to be on the side of the insurance companies with most issues. Will he look the other way?

Thought For The Day

Whoever is detected in a shameful fraud is ever after not believed even if they speak the truth.

—Phaedrus

___________________________________

1 SFR Services v. United Prop. & Cas. Ins. Co., No. 8:22-cv-00109 [Complaint] (M.D. Fla.).