As many readers may know, I live in Southeast Florida with my family and work out of the West Palm Beach office when I am not handling out of state claims/cases in other parts of the country. Over the past year , I have received numerous mailings from People’s Trust Insurance Company, like many other Florida policyholders. I thought I would write about the most recent marketing material I received from People’s Trust and how it could entice policyholders into switching to People’s Trust—but is the material somewhat deceiving to the untrained eye?

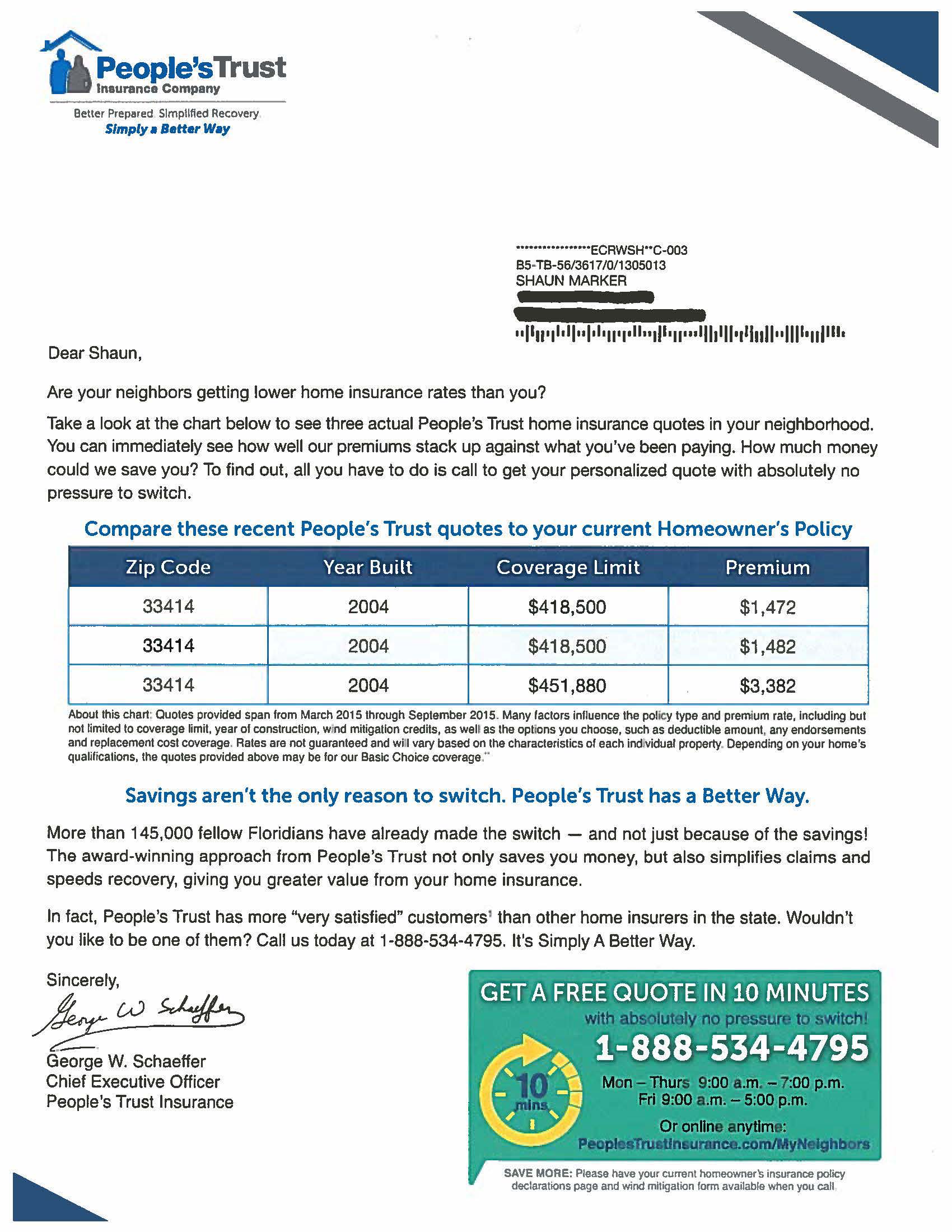

It appears to be so to me. We are lawyers so we are used to reading fine print—things that many non-lawyers do not care to read. You almost need to be a lawyer that finds their way around the fine print to make sense of this mailer and not be deceived by the enticing bottom line quote premium savings it promises! When you follow around the asterisks and numbers contained after statements in the marketing mailer down to the legend it is quite interesting. It certainly makes strong statements to save money on the premium by giving specific examples of real People’s Trust premium quotes in my neighborhood that are a fraction of what I pay for my property insurance—and this letter comes right from the CEO of People’s Trust! Here is a picture of the mailer:

.jpg)

The mailer gives three quotes of “actual people’s trust home insurance quotes in my neighborhood.” Two example quotes are a fraction of the other one and a fraction of the premium I pay for insurance with a different carrier than People’s Trust.

So instead of just discarding this mailer, I looked into it more. When you look at the statement in fine print below the chart on the mailer it states that the quotes provided may be for “Basic Choice coverage.” So what is “Basic Choice coverage” you say? When you follow the asterisk to the bottom of the back page, it states:

**Important note: Basic Choice provides coverage in the event of a catastrophic loss, such as fire or windstorm. It does NOT cover water damage, theft, vandalism, and some other perils. Please consult with your sales representative or agent to determine the best type of insurance for you.

The mailer does contain that caveat and statement within the fine print on the very bottom of the back page of the mailer, but I question whether many people if they are enticed by this premium quote example from others in the neighborhood would ever even read the fine print.

I see policyholders that aren’t aware of coverages ending up with policies providing very limited or basic coverage and they often do not realize what they have until they are unfortunate enough to sustain a loss for which they have to file a claim. I can offer a tip to avoid this situation: Do not bottom line shop for insurance! You may pay greatly if you suffer a loss and find out that you have been duped by marketing mailers and do not have the scenario evaluated by an experienced professional.